Driving Portfolio Value via Demand Maps

Driving Portfolio Value via Demand Maps

A strong brand portfolio is the engine of value creation

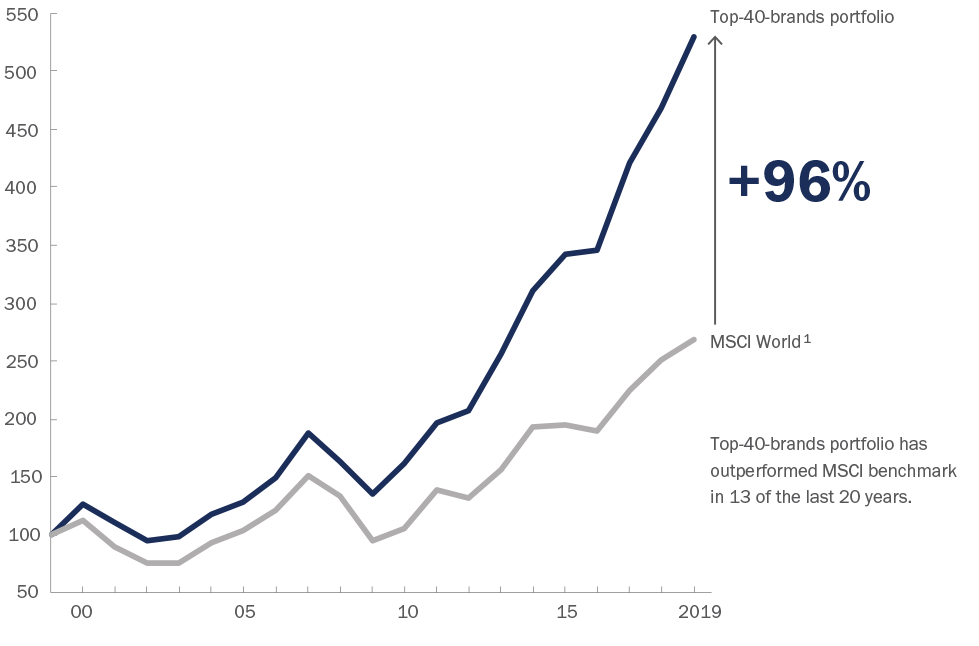

The value of a consumer goods or services company is intrinsically linked to the value of its brand or portfolio. Brand equity is rooted in how meaningful, different, trusted, and salient the brand is perceived to be by consumers. Companies with a strong brand portfolio significantly and consistently outperform the market.

A recent McKinsey study confirms this phenomenon: the world’s 40 strongest brands returned 96% more to shareholders than investment in a global market index.

Powerful brands significantly outperform the market.

Total return to shareholders, Index

While it’s clear brand value drives economic value, building a valuable brand is easier said than done, and the market is cluttered with failed or under-performing brands. In our collective experience working with hundreds of brands, we’ve found the number one determinant of success is firmly placing the consumer at the center of all brand strategy decisions. To build a strong portfolio companies must follow a structured approach that details consumer demand drivers, the role of their brands in consumers’ lives and potential for change moving forward.

Demand Maps

A critical tool for manufacturers to position individual brands and their portfolio is a demand map that captures consumer insight on key drivers of choice.

Definition:

Demand maps provide a quantified, holistic understanding of how consumers make choices. They capture who, why and how consumers engage with brands, and predict how consumption will evolve over time.

How your brands could benefit:

Demand maps drive portfolio strategy on where to play, how to action and how to win in addition to informing forward-looking innovation and acquisition decisions.

How they’re developed:

Demand maps blend primary consumer research with category-wide market data to create a multi-dimensional understanding of the space and surfaces which benefits, attributes and brand levers create the greatest sales impact (and the highest growth potential).

How to use a Demand Map

It’s important to keep in mind that demand maps vary by category given consumer drivers are often very different.

At a high-level, demand maps can be defined by occasions (the when, where, and with whom), the needs / motivations that those occasions necessitate (the why), along with the consumer cohort most likely to make a choice (the who).

Demand maps enable a brand portfolio to maximize value creation opportunities. This in turn facilitates strategic alignment across your organization.

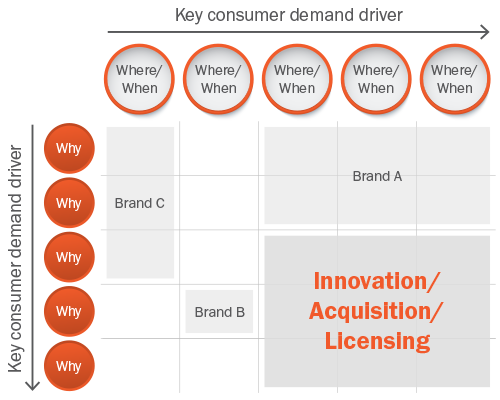

Below are our Portfolio Management Principles to leverage your Demand Map effectively:

![]() Prioritize brand lanes based on attractiveness (e.g. profit potential), brand right to win (e.g. brand’s ability to deliver on key needs), marketplace coverage (e.g. available consumption), and execution potential (e.g. brands ability to commercialize).

Prioritize brand lanes based on attractiveness (e.g. profit potential), brand right to win (e.g. brand’s ability to deliver on key needs), marketplace coverage (e.g. available consumption), and execution potential (e.g. brands ability to commercialize).

![]() Evaluate the ability for brands within the portfolio to extend across the demand map. Considerations include:

Evaluate the ability for brands within the portfolio to extend across the demand map. Considerations include:

- Covering more spaces drives penetration but risks lower salience / relevance (Brand A)

- Anchoring in one space drives loyalty & distinctiveness at the risk of reduced scale (Brand B)

- Creating clear demand lanes for each brand

![]() Cover demand spaces where company brands can’t stretch and competitors lack a right to play / win through innovation, acquisition or licensing strategies

Cover demand spaces where company brands can’t stretch and competitors lack a right to play / win through innovation, acquisition or licensing strategies

How Demand Maps come to life

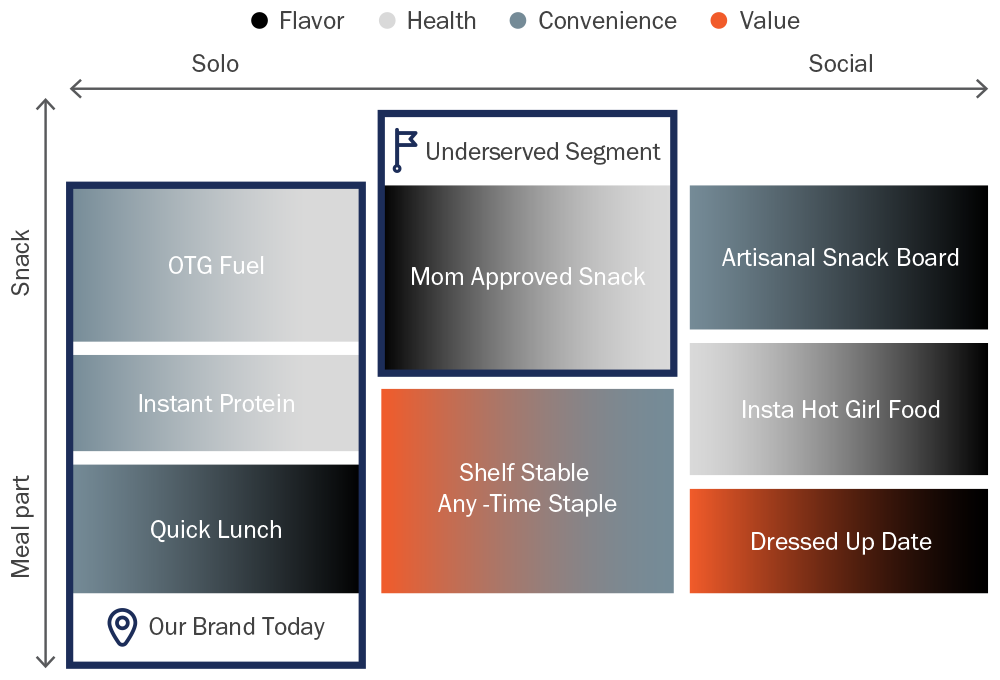

A legacy brand in the portable protein space came to Seurat after a new player entered the category that was able to tap into an entirely new consumer segment (Gen Z and Millennial women).

Seurat created a demand map to understand the category and unlock pockets of growth for our client to regain share. Our research unearthed that consumer needs for protein are largely driven by a combination of occasion and need. The category exists along two key occasion-based dimensions: snack vs. meal part and solo vs. social consumption. We then pulled apart dimensions further to uncover four distinct drivers (flavor, health, convenience and value) that mapped across 8 unique demand spaces.

After identifying key demand spaces within the category, brands can strategically position to capture new spaces.

Our work quickly revealed a sizable, underserved demand space: mom-approved snacks. By maintaining adherence to a handful of core portfolio management principles, our client was able to regain share by utilizing the demand map’s forward-looking insight to optimize their portfolio.

What Next

Are you looking to optimize your portfolio strategy?

Are you looking to solidify positioning for key brands? Could your organization benefit from demand map insights? We welcome conversation at info@seuratgroup.com