Amazon Whole Foods Acquisition

Amazon Whole Foods Acquisition

Amazon Whole Foods Acquisition

In Whole Foods Acquisition, Amazon is Accelerating the Future of Fresh Online

Fresh has a massive untapped upside online, but Amazon’s “be everywhere, sell everything” model is misaligned with shoppers’ distinct needs for an inspiration-driven online grocery experience in this space.

Amazon will need to re-orient their search-driven strategy to exploit the online fresh opportunity. The Whole Foods acquisition enables this re-orientation around a curated browse, helping consumers discover products similar to the in-store experience.

From Search …

Fresh has a massive untapped upside online, but Amazon’s “be everywhere, sell everything” model is misaligned with shoppers’ distinct needs for an inspiration-driven online grocery experience in this space.

… To Curated Browse

Fresh has a massive untapped upside online, but Amazon’s “be everywhere, sell everything” model is misaligned with shoppers’ distinct needs for an inspiration-driven online grocery experience in this space.

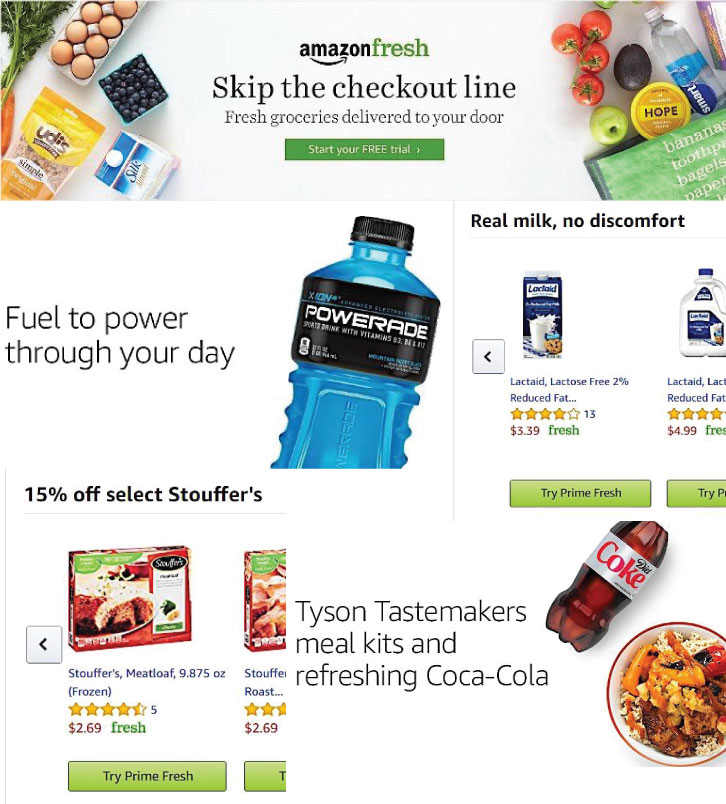

Amazon Fresh

Featuring* yesterday’s products to fulfill today’s needs  *Featured products, AmazonFresh 6/16/17 2

*Featured products, AmazonFresh 6/16/17 2

Amazon Fresh

Featuring* yesterday’s products to fulfill today’s needs

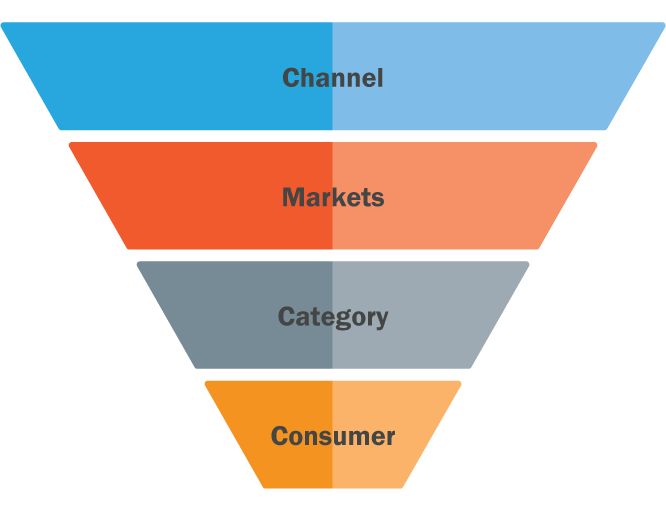

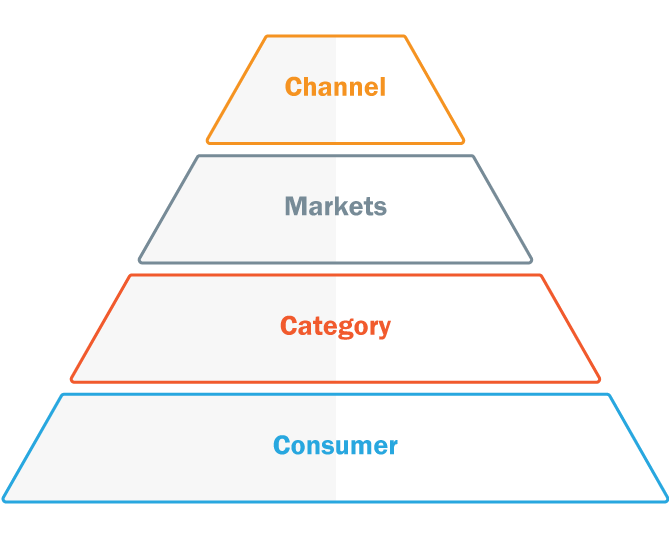

From Channel-led to Consumer-driven Strategy

Amazon was beginning with their superior online supply chain and platform, going broad to attract today’s AmazonFresh consumer.

Acquisition of Whole Foods provides an opportunity to flip the AmazonFresh pyramid. Whole Foods gives access to a wealth of consumer insights and data that has been kept secretive and reveals forward-looking CPG trends.

From Channel-led to Consumer-driven Strategy

If Amazon replicates what Whole Foods has done best in store for online grocery, manufacturers should anticipate the following changes:

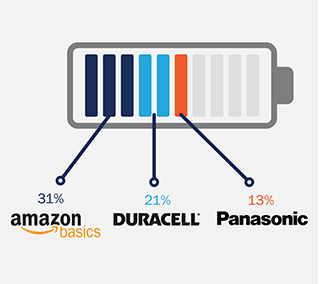

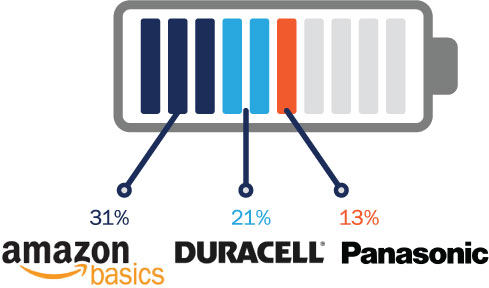

Trusted in fresh foods, Whole Foods 365 brand has the opportunity to transform fresh categories online in the same way that Amazon did for batteries, accelerating Private Label trend.

Shift in focus towards navigation and solution centers versus search, optimized for the Consumer Decision Tree of Digital Natives.

Curation of brands offered online, with a focus on fresh, local and experiential Challenger Brands with clean, healthy credentials.

Expansion of grocery and non-grocery Amazon delivery capabilities through Whole Foods real estate footprint.

Batteries eCommerce Brand Share ($)

485 “distribution centers” in locations targeting core consumer